February 2022 - Market Commentary

Assessing the Geopolitical Climate

We trust that this client letter finds you and your family in good health.

Given the recent movements in the geopolitical landscape and potential market pressure we wanted to update you with our recent thoughts. While the situation in Russia and Ukraine remains fluid, today’s news (2/22) reflects a relatively more aggressive tactical move and rhetoric from Russian President Vladimir Putin. In response, the allies have condemned Putin’s actions and rhetoric and announced new financial and economic sanctions against Russia.

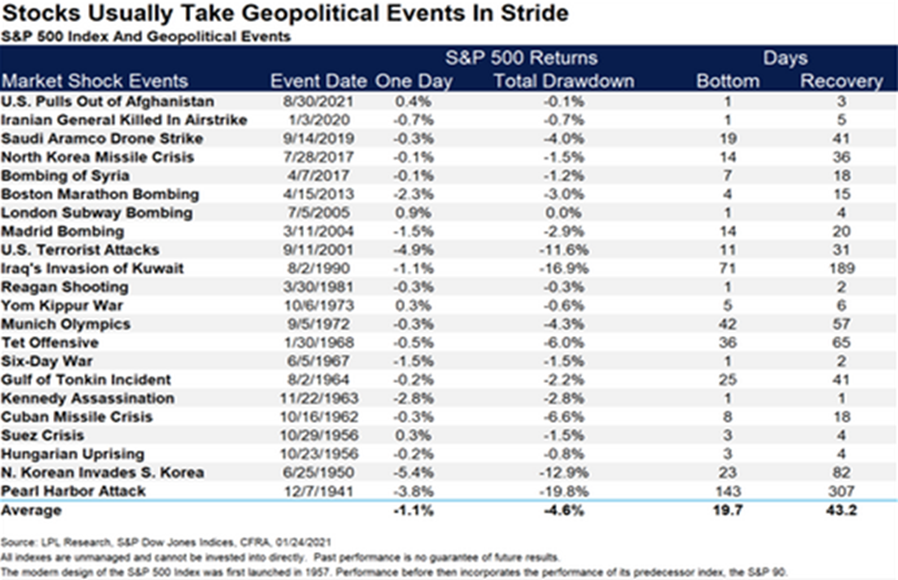

While this Russian aggression is unsettling from a geopolitical and human perspective, conflicts such as this historically have not triggered a bear market when the U.S. economy is healthy. Ryan Detrick, chief market strategist at LPL Financial, recently said “You can’t minimize what this news could mean on that part of the world and the people impacted, but from an investment point of view we need to remember that major geopolitical events historically haven’t moved stocks much,” and referenced the data below.

While there are potential implications for global commodity markets and certain U.S. sectors, Ukraine’s GDP (2020) is relatively small at $155.6B according to World Bank compared to a U.S. economy at $20.9T or 0.7%. As a result, we believe U.S. corporate earnings should be mostly insulated from a minor incursion into Ukraine.

Given the strength of growth and inflation in 2021, the Federal Reserve has shifted to a more hawkish tone over the last three months, and some analysts are now anticipating 5 to 9 interest rate increases in 2022. Additionally, the Federal Reserve has announced plans to reduce the amount of new money supply going into the U.S. economy. The recent elevated inflation data supports the Fed’s shift in policy, and we await any news if the Ukraine situation will alter the path of interest rate increases this year.

Fiscal policy remains in stall mode with low probability of new stimulus being passed by Congress in the near term. Mid-term elections may shift policy more contractionary if Republicans return one or both houses of Congress. While this may be a net drag on GDP growth, we believe improved supply-chain and logistical issues could be alleviated as businesses learn to cope with labor shortages and high wages – providing an offset to the fiscal drag. Excluding massive escalations from Ukraine, improving supply-chain dynamics could loosen U.S. inflation pressure and combined with a gradual tightening of monetary policy, the U.S. could conclude 2022 on firm footing.

The further escalation in Russia and Ukraine will most certainly impact the market in the short term and continue the volatility we have experienced since the beginning of 2022. Even though portfolios are built for long-term goals, should opportunities arise we would adjust portfolio positioning to make changes where we see appropriate.

Please reach out to your Benchmark Advisory Team with any questions or comments.