March 2026- Market Commentary

Date: March 2026

From: Investment Committee

Subject: Market commentary

______________________________________________________________________

Market Leadership Broadens as Rotation Continues

Monthly Market Summary

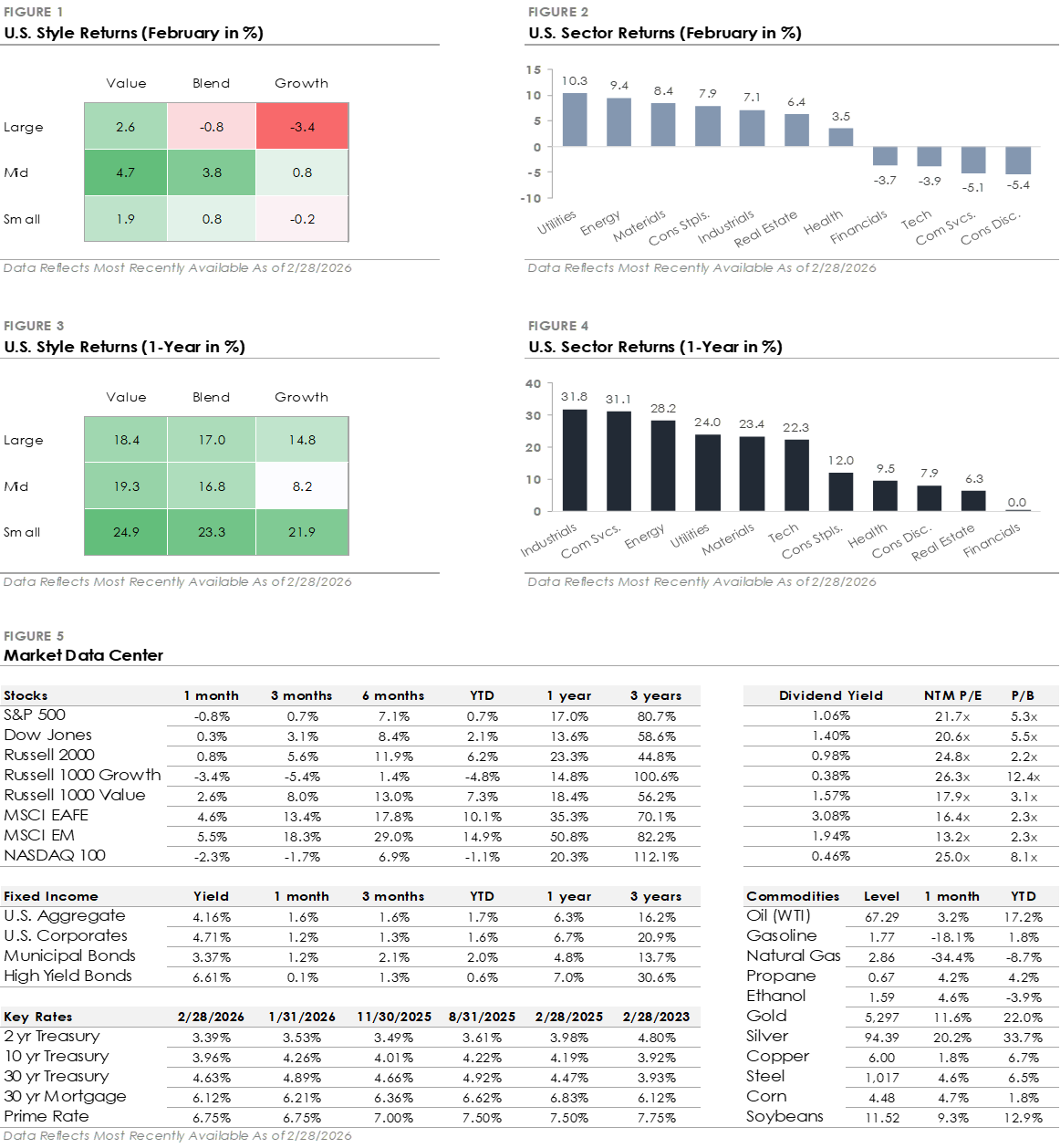

- The S&P 500 Index declined -0.8% in February, but the headline masked broad underlying strength. The equal-weighted S&P 500 gained +3.5%, Large Cap Value rose +2.6%, and the Russell 2000 added +0.8%, as the rotation toward smaller and more value-oriented companies continued. In contrast, Large Cap Growth declined -3.4% and the Nasdaq fell -2.3% as technology stocks came under pressure.

- Utilities led all S&P 500 sectors with a +10.3% return, followed by Energy (+9.4%), Materials (+8.4%), Consumer Staples (+7.9%), and Industrials (+7.1%). Seven sectors outperformed the index, while the remaining four underperformed.

- Bonds traded higher as Treasury yields declined, with the U.S. Bond Aggregate returning +1.6%. Corporate bonds traded higher, with investment-grade outperforming high-yield, but underperformed as credit spreads widened.

- International stocks outperformed the S&P 500 for a third consecutive month, with Developed Markets gaining +4.6% and Emerging Markets returning +5.5%.

Market Leadership Continues to Broaden Amid Questions About AI’s Impact

The rotation away from mega-cap tech stocks that started in January extended into February. While the S&P 500 traded lower, the average stock, as measured by the equal-weighted index, gained over +3%. The rotation was broad-based: small caps outperformed large caps, value beat growth, seven of eleven sectors beat the S&P 500, and international stocks outpaced U.S. stocks. Market leadership is broadening after a long period in which a small group of mega-cap tech stocks drove most of the market’s gains, and diversified portfolios are benefiting from the rotation.

The technology sector’s weakness was tied to concerns that artificial intelligence will impact, and potentially disrupt, current business models. A wave of AI product launches caused investors to rethink not only the potential winners, but also which industries could face disruption, such as software, consulting, real estate services, freight brokers, and other industries where AI capabilities are advancing rapidly. The selling and volatility were most pronounced early in the month but later stabilized as the narrative shifted toward a more balanced view of AI as a tool that enhances existing businesses rather than replaces them. The disruption fears eased into month-end, but investors are likely to remain focused on AI's impact on industries beyond technology.

Bonds & Gold Trade Higher as Investors Seek Stability

February was a strong month for bonds, as the 10-year Treasury yield fell nearly -0.30% to end the month below 4.00%, the lowest since October. The decline in Treasury yields drove the bond market rally, with longer-maturity and higher-quality bonds outperforming as investors sought stability amid tech sector volatility, trade policy uncertainty tied to the Supreme Court’s tariff ruling, and rising geopolitical tensions with Iran. Long-duration Treasuries gained +4.1%, and mortgage-backed securities returned +1.6%, both outperforming the broad U.S. Bond Aggregate Index.

The bond rally is notable because it occurred even as expectations for interest rate cuts were pushed further out. The Federal Reserve held interest rates steady at its January meeting after cutting in December, and the market doesn’t expect the next rate cut until June, at the earliest. The distinction is important: falling Treasury yields reflected investor demand for lower volatility assets amid the tech sector sell-off and geopolitical tensions, not a signal that economic conditions are deteriorating. Gold gained more than +10% in February, reflecting the same demand for portfolio protection.

Minutes from the Fed's January meeting signaled a continued focus on controlling inflation, and the economic data supports the Fed's patience. The labor market added +130,000 jobs in January, the unemployment rate declined to 4.3%, and an index of manufacturing activity crossed back into expansion for the first time in nearly a year. Inflation continues to ease, with core CPI rising at a +2.5% annual rate, the slowest since early 2021. The combination of steady growth and cooling inflation gives the Fed room to remain on hold. While the market still expects the Fed to cut twice this year, the start date keeps drifting later.

Where Markets Stand Today

February was a busy month filled with AI headlines, shifting market leadership, and policy uncertainty. But beneath the surface, the economic backdrop remains stable, and the Federal Reserve remains patient. As leadership broadens beyond a narrow group of mega-cap stocks, diversified portfolios are beginning to benefit from a healthier market structure.

Firm Disclosures

The information provided herein is for general informational purposes only and is intended for your personal use and should not be circulated to any other person without our permission and any use, distribution, or duplication by anyone other than the recipient is prohibited. No portion of this commentary is to be construed as an offer or solicitation to buy or sell a security, or the rendering of personalized investment advice. The views and strategies described herein may not be suitable for all investors and are subject to investment risks. The content is developed from sources believed to be providing accurate information. The information contained herein should not be relied upon in isolation for the purpose of making any investment decision.

We believe the information contained in this material to be reliable and have sought to take reasonable care in its preparation and conducted reasonable due diligence to ensure the third parties’ performance is not materially inflated or incorrect; however, we do not represent or warrant its accuracy, reliability, or completeness, or accept any liability for any loss or damage (whether direct or indirect) arising out of the use of all or any part of this material. We do not make any representation or warranty regarding any computations, graphs, tables, diagrams, or commentary in this material which are provided for illustration/ reference purposes only. These views, opinions, estimates, and strategies expressed in it constitute our judgement based on current market conditions and are subject to change without notice. Any projected results and risks are based solely on hypothetical examples cited, and actual results and risks will vary depending on specific circumstances. Investors may get back less than they invested, and past performance is not a reliable indicator of future results.

Data which may be found in this document is based on our research and should not be taken as a forecast or an estimate of likely future returns. Any reference to a market index is included for illustrative purposes only, as an index is not a security in which an investment can be made.

Investments involve some sort of risk including potential loss of principal; diversification alone cannot guarantee against loss. Any projected results and risks are based solely on hypothetical examples depicted. Forward-looking statements should not be considered guarantees or predictions of future events. More complete information is available, including product profiles, which discuss risks, benefits, liquidity, and other matters of interest. The value of any investment may fluctuate as a result of market changes. Past performance is no guarantee of future results, and there can be no assurance the investment strategies discussed herein will prove profitable.

All opinions, estimates, investment strategies and views expressed in this document are subject to change without notice information. The recommendations made for your customized portfolio may differ from any asset allocation or strategies outlined in this document. Benchmark Financial does not guarantee the future performance of any portfolio, guarantee any specific level of performance, or guarantee any strategy or overall management will be successful or that the client’s investment objectives will be met.

Benchmark Financial is not a broker dealer and does not offer tax or legal advice. Please consult your tax or legal advisor for assistance regarding your individual situation. Investment Advisory Services offered through Benchmark Financial Wealth Advisors LLC, an SEC Registered Investment Advisor. Insurance services offered through Benchmark Financial Insurance LLC. The Benchmark Financial Wealth Advisors ADV Form 2A, 2B & Form CRS, which describe the services offered, fees charged and any conflicts of interest, are available upon request or online at www.bfllc.com. Additional information about Benchmark Financial and our advisors is also available online at https://adviserinfo.sec.gov/firm/summary/287966.