May 2026- Market Commentary

Date: May 2026

From: Investment Committee

Subject: Market commentary

______________________________________________________________________

Stocks Set New Highs as Geopolitical Tensions Ease

Monthly Market Summary

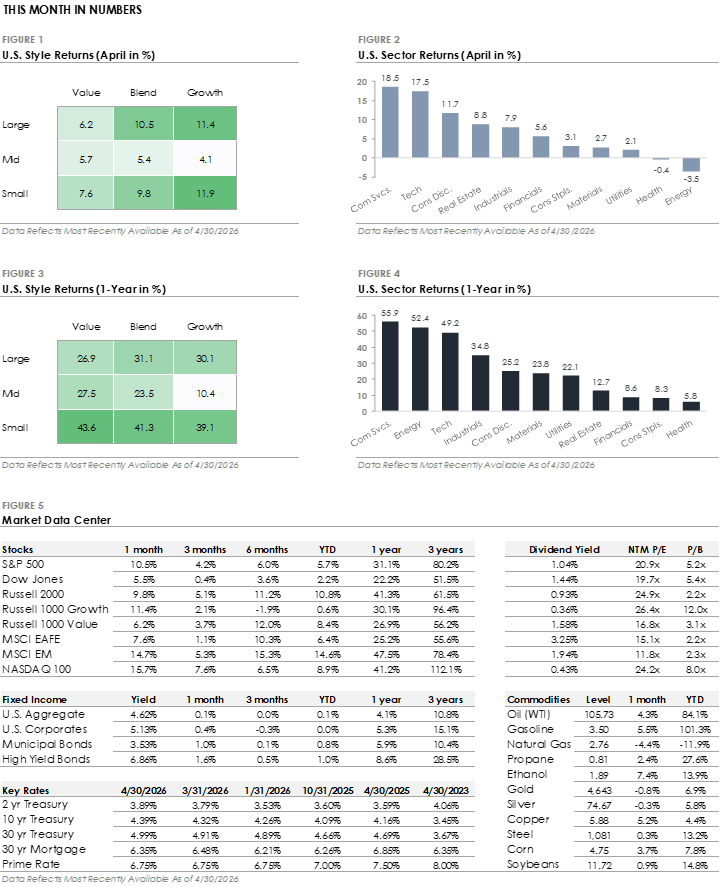

- The S&P 500 Index gained +10.5% in April, recovering its March decline and setting a new high. Communication Services led all S&P 500 sectors with a +18.5% return, followed by Technology (+17.5%) and Consumer Discretionary (+11.7%). Nine of eleven sectors traded higher as stocks recovered from the March selloff, but eight sectors underperformed the index as mega-cap stocks drove the bulk of the gains.

- Bonds traded lower as Treasury yields rose during the month. The U.S. Bond Aggregate returned +0.1% and underperformed corporate bonds as credit spreads tightened. High-yield’s +1.6% total return outpaced investment-grade’s +0.4% return as credit spread tightening benefited lower-quality bonds.

- International stocks underperformed the S&P 500 as U.S. Growth stocks led during the recovery. Emerging markets gained +14.7% and outperformed developed markets’ +7.6% return, with energy-importing regions like Europe and Japan impacted by the continued oil supply disruption.

Markets Rebound as Geopolitical Tensions Ease

Back-to-back ceasefires, first between the U.S. and Iran on April 7 and then between Israel and Lebanon on April 16, changed the market's outlook. The agreements removed the worst-case scenario, and the reversal was immediate across markets. The S&P 500 erased all its March losses and went on to set a new all-time high by month-end. The Dow surged over 1,300 points the day the U.S.-Iran ceasefire took effect, its best day in a year. The Nasdaq Index gained nearly +16% during the month, driven by a historic semiconductor rally, and the Russell 2000 small-cap index gained +9.8% and set its own record. The recovery also reached beyond stocks. Credit spreads, which reflect how concerned the bond market is about corporate borrowers, reversed three months of widening in four weeks, and market uncertainty, as measured by the VIX Index, fell to pre-conflict levels.

The relief was broad and fast, but the underlying situation remains unsettled. The Strait of Hormuz, which carries roughly 20% of global oil supply, remains effectively closed, with only a few tankers crossing daily compared to hundreds before the conflict. Oil prices fell sharply on the ceasefire announcements, including the largest single-day decline since 2020, but have since risen back above $100 per barrel. Gasoline remained above $4 a gallon throughout April, and consumer confidence fell to its lowest reading in the University of Michigan survey's 70-year history. The ceasefires reduced fears of further near-term escalation, and investors moved quickly to price that in. However, the oil supply disruption that’s become a part of the conflict has not been resolved.

AI Is Creating Winners and Losers Within the Tech Sector

The technology sector gained nearly +18% in April, but the gap between its strongest and weakest corners was wide. The divergence is being driven by artificial intelligence, which is simultaneously fueling demand in one part of the sector and raising fundamental questions about another. AI requires massive upfront investment to build and operate, including computer chips, data centers, power generation, and networking equipment. The companies that build the infrastructure are seeing a surge in demand as the physical backbone behind AI is constructed. At the same time, AI is advancing to the point where it can perform tasks that traditionally require human users interacting with software. AI agents, automated systems that can handle workflows like customer service, data entry, and internal reporting, are raising questions about the future of enterprise software.

The divergence could be seen in markets during April. Semiconductor stocks, which sell computer chips, rose more than +40% over 17 consecutive trading days, the longest uninterrupted winning streak for the group dating back to the early 1990s. Semiconductor funds absorbed $5.5 billion in new investment during the month, and earnings results from major chipmakers confirmed that infrastructure spending is translating into revenue growth. Enterprise software moved in the opposite direction. Several of the largest names in the industry have declined more than -30% this year, and the selling has even hit companies that beat earnings estimates and raised their forward guidance. The divergence comes as the market works through which business models AI will enhance and which it will disrupt. It's a question likely to define not only the technology sector but also the broader market for some time.

Firm Disclosures

The information provided herein is for general informational purposes only and is intended for your personal use and should not be circulated to any other person without our permission and any use, distribution, or duplication by anyone other than the recipient is prohibited. No portion of this commentary is to be construed as an offer or solicitation to buy or sell a security, or the rendering of personalized investment advice. The views and strategies described herein may not be suitable for all investors and are subject to investment risks. The content is developed from sources believed to be providing accurate information. The information contained herein should not be relied upon in isolation for the purpose of making any investment decision.

We believe the information contained in this material to be reliable and have sought to take reasonable care in its preparation and conducted reasonable due diligence to ensure the third parties’ performance is not materially inflated or incorrect; however, we do not represent or warrant its accuracy, reliability, or completeness, or accept any liability for any loss or damage (whether direct or indirect) arising out of the use of all or any part of this material. We do not make any representation or warranty regarding any computations, graphs, tables, diagrams, or commentary in this material which are provided for illustration/ reference purposes only. These views, opinions, estimates, and strategies expressed in it constitute our judgement based on current market conditions and are subject to change without notice. Any projected results and risks are based solely on hypothetical examples cited, and actual results and risks will vary depending on specific circumstances. Investors may get back less than they invested, and past performance is not a reliable indicator of future results.

Data which may be found in this document is based on our research and should not be taken as a forecast or an estimate of likely future returns. Any reference to a market index is included for illustrative purposes only, as an index is not a security in which an investment can be made.

Investments involve some sort of risk including potential loss of principal; diversification alone cannot guarantee against loss. Any projected results and risks are based solely on hypothetical examples depicted. Forward-looking statements should not be considered guarantees or predictions of future events. More complete information is available, including product profiles, which discuss risks, benefits, liquidity, and other matters of interest. The value of any investment may fluctuate as a result of market changes. Past performance is no guarantee of future results, and there can be no assurance the investment strategies discussed herein will prove profitable.

All opinions, estimates, investment strategies and views expressed in this document are subject to change without notice information. The recommendations made for your customized portfolio may differ from any asset allocation or strategies outlined in this document. Benchmark Financial does not guarantee the future performance of any portfolio, guarantee any specific level of performance, or guarantee any strategy or overall management will be successful or that the client’s investment objectives will be met.

Benchmark Financial is not a broker dealer and does not offer tax or legal advice. Please consult your tax or legal advisor for assistance regarding your individual situation. Investment Advisory Services offered through Benchmark Financial Wealth Advisors LLC, an SEC Registered Investment Advisor. Insurance services offered through Benchmark Financial Insurance LLC. The Benchmark Financial Wealth Advisors ADV Form 2A, 2B & Form CRS, which describe the services offered, fees charged and any conflicts of interest, are available upon request or online at www.bfllc.com. Additional information about Benchmark Financial and our advisors is also available online at https://adviserinfo.sec.gov/firm/summary/287966.