November 2025 - Market Commentary

Date: November 2025

From: Investment Committee

Subject: Market commentary

______________________________________________________________________

Stocks Hit New Highs as Market Navigates Shutdown, Fed Policy, & AI Spending

Monthly Market Summary

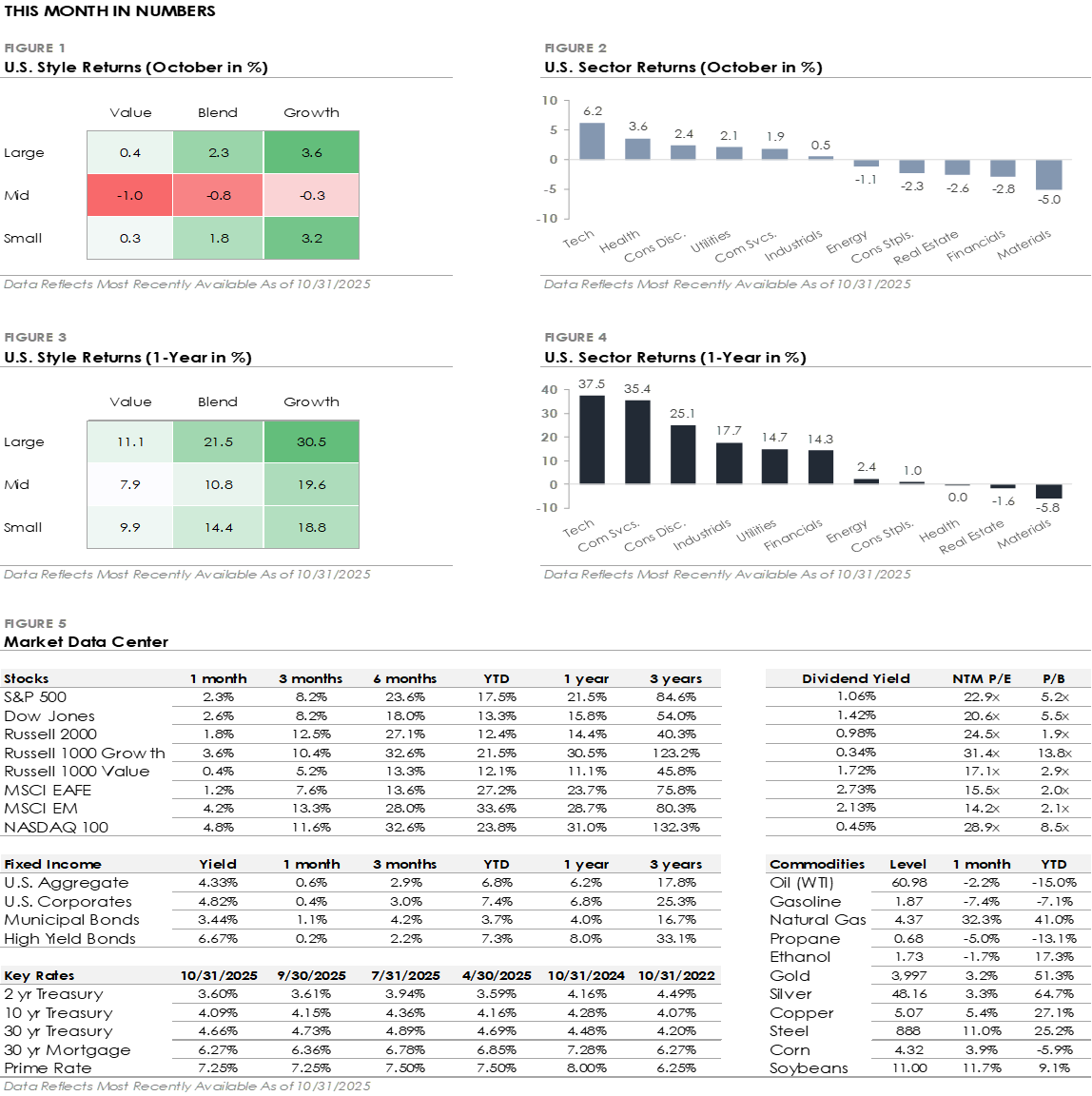

- The S&P 500 Index rose +2.3% in October, bringing its year-to-date return to +17.5%. Large Cap Growth stocks gained +3.6% and outperformed the index, while Large Cap Value returned +0.4%. Major stock indices set new highs, with the S&P 500, Dow Jones, Nasdaq 100, and Russell 2000 all posting a sixth straight month of gains.

- Technology led all S&P 500 sectors, with the Nasdaq 100 gaining +4.8%. Health Care and Consumer Discretionary also outperformed the index, while the remaining eight sectors underperformed, with five sectors trading lower.

- Bonds traded higher as Treasury yields ended lower despite intra-month volatility. The U.S. Bond Aggregate returned +0.6%, while corporate bonds underperformed. Investment-grade delivered a +0.4% total return, and high-yield gained +0.2%.

- International stocks split the S&P 500’s return. Developed Markets gained +1.2%, underperforming the S&P 500, while Emerging Markets returned +4.2%.

Federal Reserve Cuts Interest Rates as Government Shutdown Drags On

The government shutdown that began October 1st remains unresolved as of month-end, officially becoming the second-longest in U.S. history behind 2018. The shutdown, which is due to partisan gridlock over federal spending and health care subsidies, has disrupted government operations and caused hardship for federal workers. The market has mostly dismissed the stalemate as political noise, but the length of the shutdown is starting to raise concerns about its impact on consumer sentiment and business activity.

The shutdown has complicated interest rate policy by halting the release of economic data. Federal Reserve policymakers have had to make decisions without the latest data on the labor market, consumer spending, and housing market. Despite the data blackout, the Fed cut rates by -0.25% in October, its second consecutive rate cut. The decision reflects growing concern over labor market softening, with Chair Powell emphasizing that employment risks have overtaken inflation concerns, despite inflation still above the 2% target. The market expects another 0.25% rate cut in December, although the probability fell after Powell said a rate cut is “not a foregone conclusion”.

Stocks Trade Near All-Time Highs Despite Credit Concerns & Trade Tensions

Stocks ended October near all-time highs after they staged a late-month recovery. Credit concerns surfaced early in the month after multiple regional banks disclosed losses tied to commercial real estate fraud. The news came only weeks after two high-profile bankruptcies in the auto sector and reignited concerns about credit quality. Stocks initially sold off, but by month-end, concerns eased as credit rating agencies and analysts characterized the issues as isolated rather than systemic.

Around the same time, a sudden re-escalation of U.S.–China trade tensions rattled the market just weeks before a high-stakes Trump-Xi summit. It began when China expanded export restrictions on rare earth minerals, prompting the White House to threaten a 100% tariff on all Chinese imports if Beijing didn’t reverse course. The threats sparked a stock market sell-off and revived fears of a trade war. However, despite the harsh rhetoric and threats, both sides left room for negotiation. The Trump-Xi summit took place as scheduled in late October, and the meeting yielded several headline agreements that helped ease near-term U.S.-China trade tensions.

Market Sentiment: Cautious Optimism Ahead of Year-End

Market sentiment is cautiously optimistic heading into the final two months of the year, supported by the Fed’s rate-cutting cycle, continued enthusiasm around AI, and solid Q3 corporate earnings. November and December are historically strong for equities, and while investors are bullish, they’re not euphoric. Despite credit concerns fading and trade tensions easing, other risks remain. Valuations are elevated, investors are questioning the return from AI infrastructure spending, and job growth has slowed in recent months. Chair Powell’s pushback against a December rate cut tempered some enthusiasm, but hopes for a year-end market rally remain intact, even as attention shifts to 2026.

Firm Disclosures

The information provided herein is for general informational purposes only and is intended for your personal use and should not be circulated to any other person without our permission and any use, distribution, or duplication by anyone other than the recipient is prohibited. No portion of this commentary is to be construed as an offer or solicitation to buy or sell a security, or the rendering of personalized investment advice. The views and strategies described herein may not be suitable for all investors and are subject to investment risks. The content is developed from sources believed to be providing accurate information. The information contained herein should not be relied upon in isolation for the purpose of making any investment decision.

We believe the information contained in this material to be reliable and have sought to take reasonable care in its preparation and conducted reasonable due diligence to ensure the third parties’ performance is not materially inflated or incorrect; however, we do not represent or warrant its accuracy, reliability, or completeness, or accept any liability for any loss or damage (whether direct or indirect) arising out of the use of all or any part of this material. We do not make any representation or warranty regarding any computations, graphs, tables, diagrams, or commentary in this material which are provided for illustration/ reference purposes only. These views, opinions, estimates, and strategies expressed in it constitute our judgement based on current market conditions and are subject to change without notice. Any projected results and risks are based solely on hypothetical examples cited, and actual results and risks will vary depending on specific circumstances. Investors may get back less than they invested, and past performance is not a reliable indicator of future results.

Data which may be found in this document is based on our research and should not be taken as a forecast or an estimate of likely future returns. Any reference to a market index is included for illustrative purposes only, as an index is not a security in which an investment can be made.

Investments involve some sort of risk including potential loss of principal; diversification alone cannot guarantee against loss. Any projected results and risks are based solely on hypothetical examples depicted. Forward-looking statements should not be considered guarantees or predictions of future events. More complete information is available, including product profiles, which discuss risks, benefits, liquidity, and other matters of interest. The value of any investment may fluctuate as a result of market changes. Past performance is no guarantee of future results, and there can be no assurance the investment strategies discussed herein will prove profitable.

All opinions, estimates, investment strategies and views expressed in this document are subject to change without notice information. The recommendations made for your customized portfolio may differ from any asset allocation or strategies outlined in this document. Benchmark Financial does not guarantee the future performance of any portfolio, guarantee any specific level of performance, or guarantee any strategy or overall management will be successful or that the client’s investment objectives will be met.

Benchmark Financial is not a broker dealer and does not offer tax or legal advice. Please consult your tax or legal advisor for assistance regarding your individual situation. Investment Advisory Services offered through Benchmark Financial Wealth Advisors LLC, an SEC Registered Investment Advisor. Insurance services offered through Benchmark Financial Insurance LLC. The Benchmark Financial Wealth Advisors ADV Form 2A, 2B & Form CRS, which describe the services offered, fees charged and any conflicts of interest, are available upon request or online at www.bfllc.com. Additional information about Benchmark Financial and our advisors is also available online at https://adviserinfo.sec.gov/firm/summary/287966.